Bundesverband Alternative Investments e.V. (BAI)

Supervisory law for investors in the fund industry refers to the prudential regulation of the respective investors themselves.

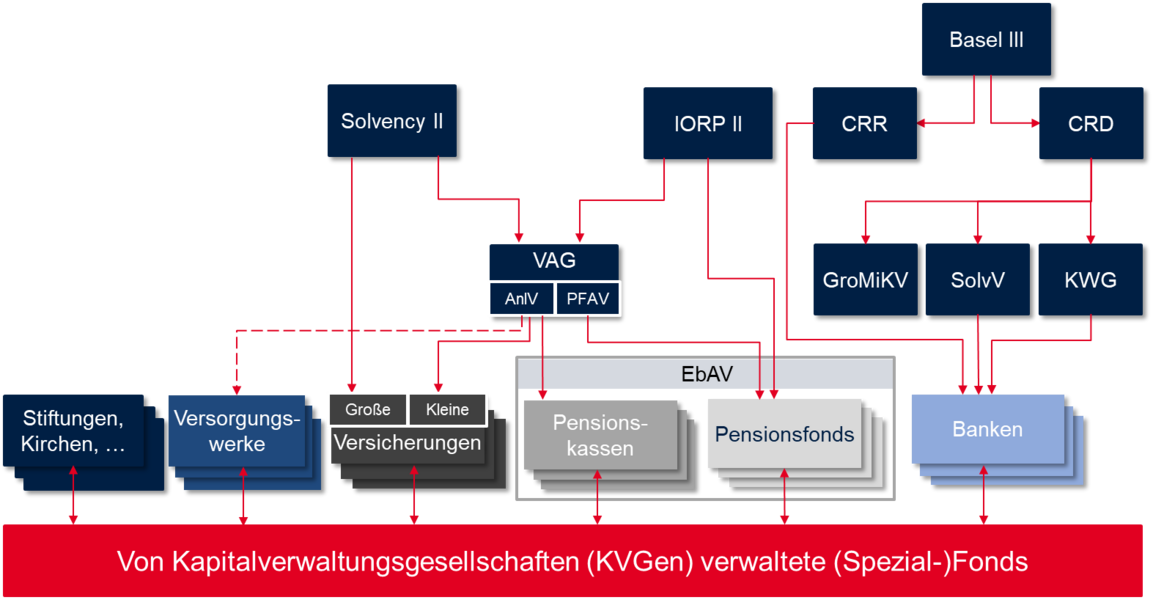

Institutional investors such as insurance companies, pension schemes, credit institutions, foundations or churches are the most important investors in open-ended special funds. They are usually themselves subject to high regulatory requirements in order to protect the respective insured persons, pension scheme members or bank customers (or the financial market and financial market stability as a whole). Where the respective investor supervision law (Solvency II for insurers, CRD/CRR for credit institutions and IORP II for pension schemes, the German Insurance Supervision Act (VAG) and the Investment Ordinance (AnlV) for small insurers or pension funds) sets regulatory requirements, fund companies (investment management companies) are indirectly affected by their respective customers: An investment management company should know the regulatory/supervisory requirements of its investors in order to offer suitable products/funds. For example, the investment management company takes over the calculation of the SCR requirement of a capital investment in accordance with Solvency II, knows about the eligibility for the quotas or "numbers" of the Investment Ordinance and takes care of the investor supervisory reporting obligations to which the investors are actually directly subject.

The following graphic overview illustrates the regulatory network into which investment management companies are indirectly involved via their customers/institutional investors, both at the level of EU law and German law.

Current Activities

EIOPA comments on sustainability risks

With the publication of a discussion paper on the macroprudential treatment of sustainability risks, EIOPA is advancing the sustainability discourse in supervisory law for investors. EIOPA regards the adaptation to these risks as a central task for insurance markets. For EIOPA, the focus is on exploring the link between tranition-related sustainability risks and macroprudential risks, adapting to climate risks in risk assesment, and strengthening the social component of ESG.

Discussion paper of EIOPA on the macroprudential treatment of sustainability risks

Banking Package 2021

In October 2021, the review of the EU banking regulation has been rung in with the adoption of proposals to amend the Capital Requirements Regulation (CRR), the Capital Requirements Directive (CRD) and the Capital Requirements Regulation in the area of resolutoin ('daisy chain' proposal). The drafts propose amendments build on top of the current supervisory regulation for banks after the Great Financial Crisis in 2008, expanding it to achieve the rebuilding of the postpandemic economy and the ecological transition.

The package is comprises of the following three core components:

- Implementing Basel III – strengthening resilience to economic shocks:

The package implements the international Basel III agreement, while taking into account the specific features of the EU's banking sector, for example when it comes to low-risk mortgages - Sustainability – contributing to the green transition:

The new rules will require banks to systematically identify, disclose and manage sustainability risks (environmental, social and governance or ESG risks) as part of their risk management - Stronger enforcement tools – ensuring sound management of EU banks and better protecting financial stability:

The package provides stronger enforcement tools for supervisors overseeing EU banks

The draft report of the Economic Council of the European Parliament (ECON) on the CRR, accompanied by numerous amendment proposals, was published on May 23 2022. The BAI published a position paper on this as well, which focused on the impact assesment regarding subordinated debt, equity and other capital instruments.

Press release of the EU commission on the banking package 2021

Text of the proposal to amend the Capital Requirements Regulation (CRR)

Text of the proposal to amend the Capital Requirements Directive (CRD)

Prudential Regulation of (large) insurers: Solvency II

(Large) insurance companies are the most important investors in special funds, about one third of the assets of open-ended special funds or roundabout 600 billion Euros originate from the insurance industry.

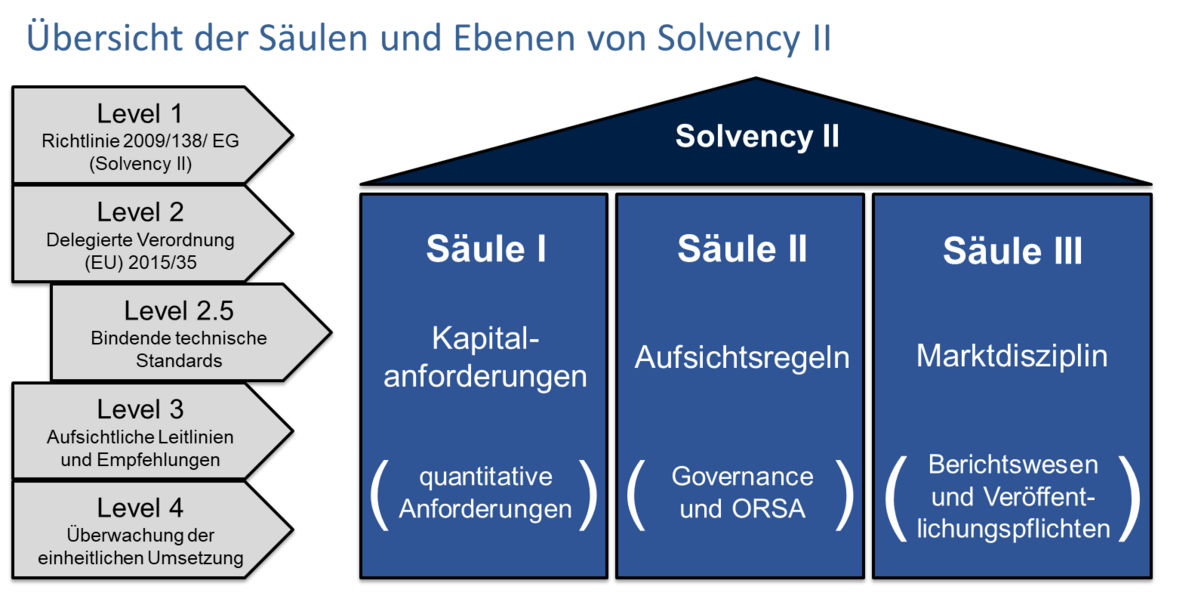

With the entry into force of Solvency II, this important market was regulated throughout Europe in 2016. The main focus lies on riskbased solvency requirements for the capital adequacy of insurance companies and qualitative requirements for the risk management of insurance companies as well as extended publication obligations.

The directive follows a three-pillar approach:

- Pillar I concerns the amount of the minimum capital requirement (MCR) and the amount of the solvency capital requirement (SCR) in relation to eligible own funds (EOF).

- Pillar II deals with the risk management system and primarily includes qualitative requirements.

- Pillar III regulates the reporting obligations of insurance companies: on the one hand, reporting obligations to supervisory authorities and, on the other, information to be published.

In addition, Solvency II contains regulations on the supervision of insurance groups. Insurance companies must calculate their Solvency Capital Requirement (SCR) in accordance with a standard formula that is uniformly applied throughout the EU and takes into account the main risks associated with the business activities of insurance companies. These own funds are designed to protect insurance companies from insolvency and to ensure that they are able to comply with their insurance contracts and to pay out customers even in the event of adverse economic conditions. Depending on the type of assets in which insurance companies invest their assets, they will have to be backed by different levels of equity. Therefore, insurance companies need to know the individual assets they are investing in, and if they are bundled in investment funds, for example in a specialized AIF with fixed investment rules, they need to be able to see through this fund structure. Accordingly, the so-called look-through approach includes the procedures for determining the market risk capital of investment funds provided for by Solvency II. Solvency II also laid down new requirements for quantitative reporting to the supervisory authorities ("Pillar III"; Pillar II contains supervisory rules for governance and ORSA). The detailed provisions on this can be found in the Solvency II Implementing Regulation (Solvency II Level II Regulation).

Solvency II review

The review process of the Solvency II Directive is currently ongoing. In September 2021, the EU Commission published a draft proposal to amend the Directive and for a new Recovery and Resolution Directive. In addition, it provided information on future amendments to the Delegated Regulation that are being considered in the course of the Solvency II review. Votes in the European Council and European Parliament are expected in the second half of 2022.

The proposal aims to make the industry more resilient allowing it to be better equipped to deal with future crises and to better protect policyholders. Simplified and more proportionate rules will also be introduced for certain smaller insurance companies.

The proposals were preceded by an extensive EIOPA consultation since 2019, which included a review of technical data and implications of the previous Solvency II directive. In July 2020, the EU Commission took on board the findings and, in conjunction with EIOPA, published the legislative proposal on September 22, 2021.

Draft proposal Recovery and Resolution of Insurance and Reinsurance Undertakings

Legal basis

Solvency II (Directive 2009/138/EC)

Solvency II Implementing Regulation (Delegated Regulation (EU) 2015/35), corrected by Delegated Regulation (EU) 2016/2283 and amended since then by Delegated Regulation (EU) 2016/467, which amended the calculation of regulatory capital requirements for various categories of investments, in particular for Qualifying Infrastructure, and by Delegated Regulation (EU) 2019/981, implementing the results of the SCR Review 2018 (first review of the standard formula).

Auf der folgenden BaFin-Seite finden sich Rechtsgrundlagen, Leitlinien und Auslegungsentscheidungen der BaFin zu Solvency II der Level 2.5 (Bindende technische Standards) und Level 3 (Aufsichtliche Leitlinien und Empfehlungen), inklusive Verweisen auf Q&A und Leitlinien der europäischen Versicherungsaufsicht EIOPA:

Rechtsgrundlagen, Leitlinien und Auslegungsentscheidungen der BaFin

Further information

The following very informative BaFin website contains bases in law, guidelines and BaFin’s interpretative decisions of on Solvency II of Level 2.5 (binding Technical Standards) and Level 3 (Supervisory Guidelines and Recommendations), including references to Q&A and guidelines of the European Insurance Supervision Authority EIOPA:

Bases in law, guidelines and interpretative decisions of BaFin on Solvency II

An interactive online graphic on Solvency II can be found on the GDV (German Insurance Association) homepage (in German only):

interactive online graphic on Solvency II

Further information can be found on the “Solvency II kompakt” homepage (in German only)

In order to meet the requirements as an “interface” between supervisors and insurers and to support insurance companies with the requirements for SCR calculation and reporting obligations, the investment industry of several countries has created the so-called "Tripartite Template (TPT) for Solvency II Asset Data Reporting". This EU fund data sheet supports and improves the exchange of data on the composition of fund portfolios between investment management companies and insurance companies.

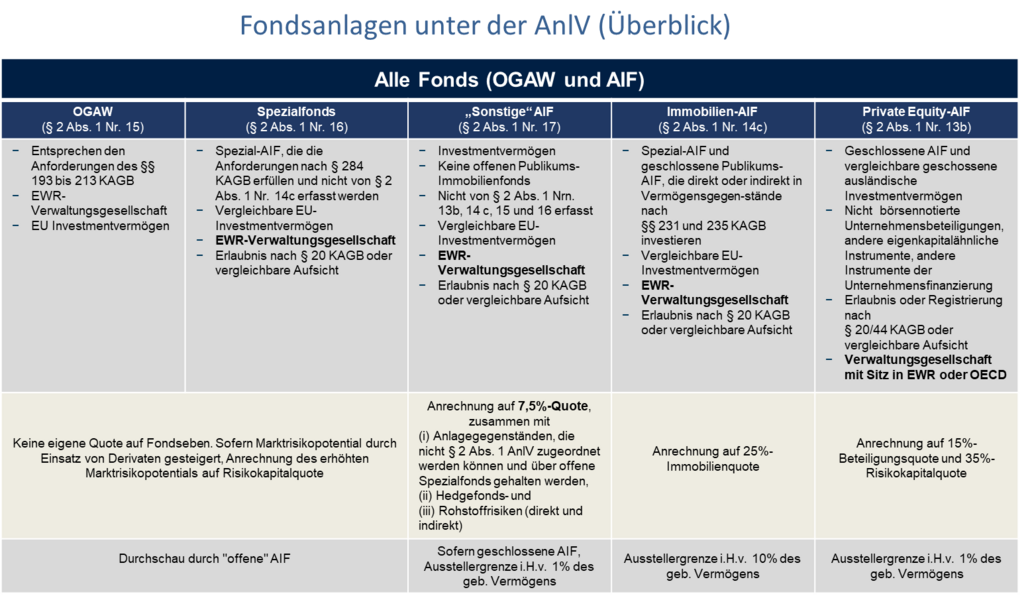

Prudential Regulation of (small) insurers: German Insurance Supervision Act (VAG)/Investment Ordinance (AnlV)/BaFin Circular to the Investment Ordinance

While "large" insurance companies are subject to Solvency II and its principle-based regulatory approach, so-called "small" insurance companies continue to be regulated only by the German Insurance Supervision Act (VAG). According to § 215 (section 215) of the VAG, the "guarantee assets in accordance with section 125 must be invested in a way that ensures the greatest possible security and profitability, while maintaining the insurance undertaking's liquidity at all times and providing an adequate mix and diversification in the portfolio.” These investment principles for the guarantee assets (“Sicherungsvermögen”) are further specified by the Investment Ordinance (AnlV) and BaFin’s Circular on the AnlV. In practice, the AnlV and the BaFin Circular are of enormous importance for institutional investors in fund structuring because questions of eligibility/qualification for the respective numbers of § 2 (1) of the AnlV and the quotas of the AnlV must be clarified before investments are made.

The following diagram provides an overview of fund investments possibilities under the Investment Ordinance (AnlV):

Prudential Regulation of „Versorgungswerke“ (pension schemes): Investment Ordinance (AnlV)/BaFin Circular 11/2017 – indirectly regulated by these acts qua law of the Länder

“Versorgungswerke” are some kind of pension funds, pension plans or pension schemes. Professional pension schemes ensure that the liberal professions of doctors, pharmacists, architects, notaries, lawyers, tax consultants and tax agents, veterinarians, auditors and certified accountants, dentists as well as engineers and psychotherapists are covered by compulsory old-age, disability and survivors' pensions.

As public-law compulsory pension schemes of "their own kind" – clearly distinguished from other pension schemes – they are based on a legal basis laid down by Land law within the exclusive legislative competence of the Länder under Article 70 of the Basic Law (“Grundgesetz”, the German Constitution).

The numerous pension schemes in the German Länder a high status as institutional investors. As public law corporations, they are supervised by the respective Länder (federal states) or state ministries. Although the pension schemes are not covered by the scope of application, the rules of the Investment Ordinance (AnlV) and BaFin’s Investment Circular 11/2017 to the Investment Ordinance are indirectly applicable in practice under state law/law of the Länder. One example is the provision in the articles of association of a pension scheme for self-employed members of a liberal profession, according to which the "assets of the pension scheme [...], insofar as they are not to be kept available to cover current expenditure, are to be invested in accordance with the principles of § 215 (1) of the Insurance Supervision Act (VAG) in the relevant version". Accordingly, the bodies of the pension schemes also indirectly apply the provisions of the Investment Ordinance (AnlV) and BaFin’s Investment Circular 11/2017 to the Investment Ordinance.

Legal basis

BaFin Circular 11/2017 to the Investment Ordinance (in German only)

Regulation of pension funds (“Pensionskassen”): IORP II/German Insurance Supervision Act (VAG)/Investment Ordinance (AnlV)/BaFin Circular to the Investment Ordinance

In many cases, occupational pension schemes are financed through direct insurance, pension funds or pension funds. The latter two are referred to for supervisory purposes as "institutions for occupational retirement provision" (in short: IOPRs). Direct insurance is offered by life insurance companies and is subject to Solvency II for supervisory purposes.

IORPs are subject throughout Europe to the EU Directive 2016/2341 (IORP II Directive, or Institutions for Occupational Retirement Provision Directive), which replaced the old directive from 2003. The IORP II Directive was transposed into German law by an amendment to the Insurance Supervision Act (VAG Part 4) on 13 January 2019 and has been in force since this date. According to § 1 (1) No. 1 of the Investment Ordinance (AnlV), the following applies to the implementation of the directive via pension funds: "This Regulation applies to the investment of guarantee assets of (a) Pensionskassen within the meaning of section 232 of the Insurance Supervision Act,, ...", why the more specific legal framework of the Investment Ordinance (AnlV) and BaFin’s Investment Circular 11/2017 for capital investments of pension funds apply.

Legal basis

IORP II Directive (Directive (EU) 2016/2341)

German Insurance Supervision Act (VAG) – convenience translation by BaFin

BaFin Circular 11/2017 to the Investment Ordinance (in German only)

Further information

Further information on the supervisory framework IORP II can also be found on the website of the “Arbeitsgemeinschaft betriebliche Altersversorgung e.V.” (aba):

Website of aba on IORP II issues

IORP II review

With a call for advice in January 2023, the EU commission has paved the way for the review of the IORP II Directive.

On March 3 2022, the EIOPA has answered this call with a draft of technical advice on IOPRP II, which it has opened for consulation. Besides general topics such as the proportionality of the regulation, its proposal envisages expansions in the area of sustainability especially. Sustanability factors should be integrated in investments decisions and taken into consideration in the fiduciary duties and management regulation of pension funds. Also, the introduction of the double materiality approach should be evaluated.

Call for advice of the EU commission on the IORP II Directive

Consultation on technical advice of EIOPA on the IORP II Directive

Prudential Regulation of pension funds: IORP II/ German Insurance Supervision Act (VAG )/Regulation on the supervision of pension funds (PFAV)

In many cases, occupational pension schemes are financed through direct insurance, pension funds or pension funds. The latter two are referred to for supervisory purposes as "institutions for occupational retirement provision" (in short: IOPRs). Direct insurance is offered by life insurance companies and is subject to Solvency II for supervisory purposes. In Germany there are around 30 pension funds which are subject to BaFin’s supervision.

IORPs are subject throughout Europe to the EU Directive 2016/2341 (IORP II Directive, or Institutions for Occupational Retirement Provision Directive), which replaced the old directive from 2003. The IORP II Directive was transposed into German law by an amendment to the Insurance Supervision Act (VAG Part 4) on 13 January 2019 and has been in force since this date.

The regulatory framework for pension funds is also being further specified at ordinance level. However, the Regulation on the supervision of pension funds (PFAV) is applicable and not the Investment Ordinance (AnlV). The provisions of the PFAV on investment principles, investment management and forms of investment are similar to those of the AnlV, but the bottom line is that they are more liberal and less rigid overall. There are significant differences to the provisions for primary insurance companies and domestic pension funds, in particular with regard to the requirements for the mix of the various forms of investment (§ 18 PFAV). In this respect, pension funds have greater freedom of investments. BaFin’s Investment Circular 11/2017 contains a section "C. Separate notes on the investment of the guarantee assets of domestic pension funds".

Legal basis

IORP II Directive (Directive (EU) 2016/2341)

German Insurance Supervision Act (VAG) – convenience translation by BaFin

PFAV (in German only)

BaFin Circular 11/2017 to the Investment Ordinance (in German only)

Further information

Further information on the supervisory framework IORP II can also be found on the website of the “Arbeitsgemeinschaft betriebliche Altersversorgung e.V.” (aba):

Regulation of banks: CRD/CRR/German Banking Act (KWG)/GroMiKV/SolvV

Banks are also important institutional investors and thus customers in (special) investment funds and account for approx. 11% of the assets of special funds. They are subject to a wide range of requirements under banking supervisory law. With the document "A global regulatory framework for more resilient banks and banking systems" of the Basel Committee on Banking Supervision, the so-called Basel III framework was adopted in December 2010, which was implemented at European level by the legislative package CRD IV/CRR. The legislative package consists of a Directive (CRD IV) and a Regulation (CRR), which replaced the previous Capital Requirements Directives. The CRD IV/CRR legislative package entered into force on 1 January 2014. In the course of the national implementation of CRD IV, the CRD IV Implementation Act has brought about a far-reaching change to the German Banking Act and to the legal regulations associated with the German Banking Act (including SolvV and GroMiKV) – being the GroMiKV the Ordinance on the Recording, Measurement, Weighting and Display of Loans in the Area of Large Exposures and Million Loans Provisions of the German Banking Act (KWG) and the SolvV Solvency Ordinance to the German Banking Act (KWG). The CRR is directly applicable.

Since 2016, drafts for the revision of the directive (then CRD V), regulation (then CRR II) and the Bank Recovery and Resolution Directive (BRRD) have been discussed. The so-called EU banking package, which includes CRD V, CRR II, BRRD II and SRMR II, was published in the Official Journal of the European Union on 7 June 2019 and entered into force on 27 June 2019.

Banks or credit institutions have to fulfil reporting obligations on capital requirements, capital deduction positions, the countercyclical capital buffer, liquidity capital requirement (LCR), risk-bearing capacity, large exposures and the investment management’s million exposure report. Investment managements are at the “interface” between investment funds and banks as investors in investment funds.

As with Solvency II and the determination of the SCR, investment companies’ bank reporting is also subject to the (indirect or, if applicable, contractual obligation) to determine risk weights according to the CRR. The look-through method for determining the risk weight for investment units in the standard approach in accordance with Art. 132 (4) CRR is used for this purpose in connection with the determination of the credit risk (Part 3 Title II Chapter 2 CRR) in the context of reporting to institutions.

Legal basis

CRD IV (Directive 2013/36/EU)

CRR (Regulation (EU) Nr. 575/2013)

CRD V (Directive 2019/878/EU amending Directive 2013/36/EU)

CRR II (Regulation (EU) 2019/876 amending Regulation (EU) Nr. 575/2013)

German Banking Act – convenience translation by BaFin

Solvency Ordinance to the German Banking Act (KWG) – in German only

Feedback statements of BAI

BAI comments on the CRR revision following the Basel-IV implementation regarding "Subordinated debt, equity and other capital instruments"

September 2021